Cycling event insurance is defined as specialized coverage that protects event organizers and participants from financial and legal risks caused by accidents, injuries, and property damage during rides and races. Understanding why cycling events need insurance is the first step every organizer must take before a single rider clips in. Two core policy types drive this protection: event liability insurance and participant accident insurance. Industry bodies like USA Cycling and Cycling BC have built insurance requirements directly into their sanctioning frameworks, which tells you everything about how serious these risks are.

Why cycling events need insurance: the core case

The financial exposure from a single accident at a cycling event can exceed what most organizers expect. Event liability insurance costs as low as $0.15 per participant, with minimum premiums around $75, yet it covers legal defense costs and third-party damages that could otherwise bankrupt an organization. That cost-to-protection ratio is one of the strongest arguments for cycling event coverage. Cycling BC’s Commercial General Liability policy offers up to $10 million in coverage for sanctioned events, extending protection to landowners and sponsors listed as Additional Insured. That scale of coverage reflects the real-world severity of claims that arise from competitive cycling.

Cycling risks and insurance go hand in hand because the sport involves speed, traffic, and unpredictable terrain. A spectator struck by a rider, a vehicle damaged in a parking area, or a course marshal injured during setup can all trigger third-party claims. Without insurance, the organizer absorbs every dollar of that exposure personally.

What types of insurance do cycling events typically require?

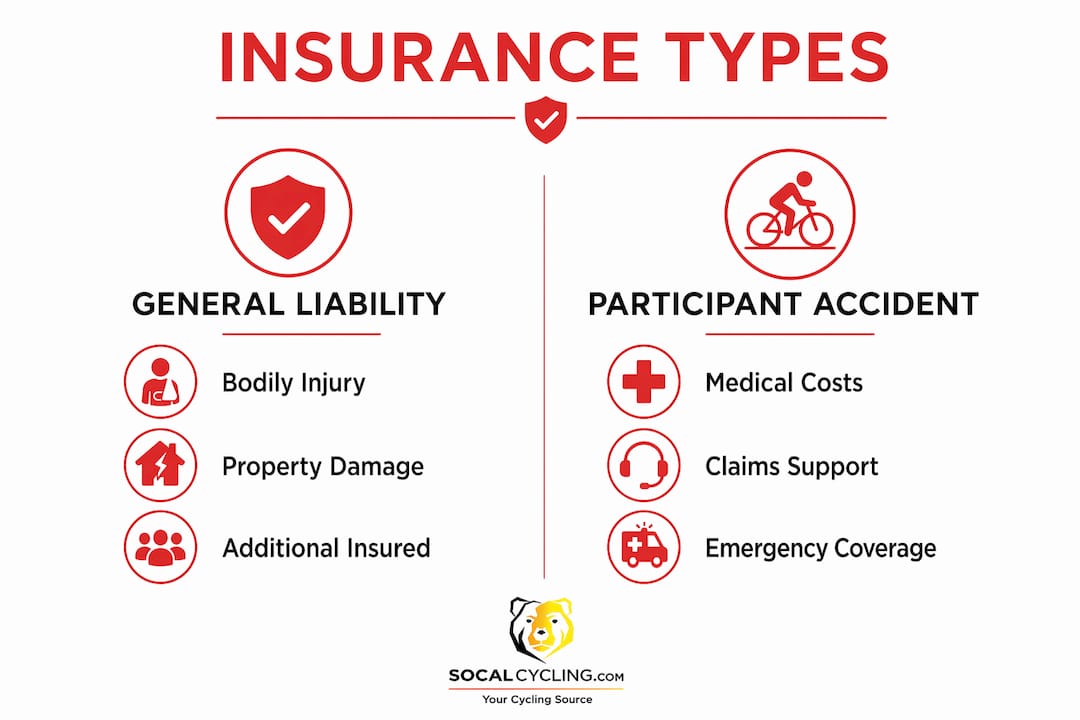

Cycling event organizers generally need two distinct policy types, and confusing them creates dangerous gaps in protection.

General liability insurance covers third-party bodily injury and property damage claims. This is the policy that protects you when a spectator is hurt or a landowner’s fence gets damaged during the event. It does not cover the medical bills of your registered participants.

Participant accident insurance fills that gap. It pays for medical expenses when a registered cyclist gets injured during the event, regardless of who is at fault. This coverage is separate from liability and addresses a completely different risk.

Beyond these two core policies, organizers should also consider:

- Event cancellation insurance: Reimburses non-recoverable costs if weather, venue issues, or other covered causes force you to cancel.

- Equipment insurance: Covers timing systems, barriers, and other event infrastructure against theft or damage.

- Directors and officers coverage: Protects board members of cycling clubs or nonprofits from personal financial exposure tied to event decisions.

Coverage limits vary significantly. A small community gran fondo might carry a $2 million aggregate limit, while a larger sanctioned race through Cycling BC can access up to $10 million. The right limit depends on your venue, participant count, and the requirements of your permit authority.

Adding Additional Insured parties is not optional in most cases. Landowners, municipalities, and sponsors routinely require it before granting venue access. Including them on your policy extends the liability protection to cover claims made against those parties in connection with your event.

Pro Tip: Always request a certificate of insurance naming your venue owner and any government agency as Additional Insured before you finalize your permit application. Missing this step is the most common reason permit approvals get delayed.

Why is event liability insurance essential for cycling event organizers?

Event liability insurance is the legal and financial backbone of any organized cycling event. Without it, a single lawsuit can expose you, your club, and every board member to personal financial ruin.

Organizers and board members can be named personally in lawsuits when event insurance is missing or insufficient. That means your personal savings, home, and assets are at risk if a claim exceeds your coverage or if you have no coverage at all. Proper Commercial General Liability insurance, tied to a sanctioned event, shields individuals from that personal exposure.

Many organizers believe that a signed participant waiver eliminates their legal risk. Waivers help, but they are not a complete defense. Signed waivers do not protect against claims involving gross negligence or incidents that fall outside the inherent risks of the sport. A poorly marked course, an unmarked hazard, or a failure to provide adequate medical support can all generate claims that a waiver will not stop.

Waivers provide a layer of defense, but courts regularly allow claims to proceed when gross negligence is alleged. Insurance is the only protection that covers legal defense costs and potential damages in those situations.

The practical risks that liability insurance addresses include:

- A spectator injured by a crash at the finish line

- A third-party vehicle damaged by a course vehicle

- A property damage claim from a landowner after the event

- A lawsuit filed by a participant who argues the course was unsafe

Each of these scenarios triggers legal defense costs before any judgment is even reached. Liability insurance covers those defense costs up to your policy limits, which is critical because legal fees alone can reach tens of thousands of dollars even when you win.

For organizers running charity cycling rides or community gran fondos, the personal liability exposure is identical to that of a professional race director. The size of the event does not reduce the legal risk.

How does participant accident insurance complement event liability coverage?

Participant accident insurance and event liability insurance solve different problems. Liability insurance defends you against claims made by injured parties. Participant accident insurance covers the medical expenses of injured cyclists directly, without requiring proof of organizer fault.

This distinction matters because most cycling crashes are caused by the rider’s own actions. Liability insurance does not pay for a participant’s broken collarbone if the crash was the rider’s fault. Participant accident insurance pays regardless of fault, which means injured cyclists get medical cost support without needing to file a lawsuit against the organizer.

The practical steps for using participant accident coverage follow a specific process:

- Seek emergency treatment immediately. USA Cycling’s participant accident policy requires emergency treatment within 72 hours of the incident for the claim to be eligible.

- Document the incident at the event. Collect witness information, photograph the scene, and file an incident report before participants leave.

- Submit all claims within 30 days. USA Cycling’s policy requires claims submitted within 30 days of the incident for coverage eligibility.

- Coordinate with your insurance provider. Provide the incident report, medical records, and any other documentation requested.

When participants know medical cost support exists, they are less likely to pursue legal action against the organizer. That dynamic reduces the overall claims burden on your liability policy and creates a better experience for everyone involved.

Pro Tip: Print the claims submission deadline and emergency treatment requirement on your participant information sheet. Injured cyclists rarely remember policy details after a crash, and a missed deadline voids the claim entirely.

A common misconception is that a participant’s personal health insurance or club membership covers racing events. Standard personal and club policies typically exclude coverage for racing and timed competitive events. Event-specific participant accident insurance fills that gap directly.

What are the practical steps to secure cycling event insurance?

Securing the right insurance for a cycling event follows a clear process. Skipping any step creates coverage gaps that expose you to uninsured risk.

Get your event sanctioned first. Sanctioning through a body like USA Cycling or Cycling BC is often the trigger that unlocks access to group insurance programs. Sanctioned events qualify for comprehensive coverage that standard policies exclude. Confirm your event’s sanctioned status before purchasing any policy.

Understand your costs. Typical event liability insurance runs around $0.15 per participant, with minimum premiums that cover legal defense and third-party damages. For a 200-person event, that puts your base liability cost well under $100, making it one of the lowest-cost risk management tools available.

The table below summarizes the key insurance types, their coverage focus, and typical considerations:

| Insurance type | What it covers | Key consideration |

|---|---|---|

| General liability | Third-party injury and property damage | Required for most venue permits |

| Participant accident | Medical expenses for registered cyclists | Requires timely treatment and claim filing |

| Event cancellation | Non-recoverable costs if event is canceled | Useful for large events with significant deposits |

| Equipment coverage | Timing systems, barriers, event infrastructure | Optional but valuable for tech-heavy events |

| Directors and officers | Personal liability for board members | Critical for nonprofit cycling clubs |

Additional steps to manage your coverage effectively:

- Add all required Additional Insured parties. Landowners, municipalities, and sponsors often require this as a condition of venue access. Including landowners and sponsors as Additional Insured is standard practice for securing permits.

- Read your policy exclusions carefully. Racing and timed events are frequently excluded from standard policies. Confirm your policy explicitly covers the format of your event.

- Keep all insurance documents with your permit file. Venue owners and permit authorities may request proof of coverage on short notice.

- Review coverage annually. Event formats, participant counts, and venue requirements change. Your policy should reflect your current event, not last year’s version.

For organizers planning events like a cycling omnium or a cyclocross race series, the insurance requirements shift based on the competitive format. Confirm the specific exclusions and requirements for your event type with your insurance provider before finalizing your program.

Key Takeaways

Cycling event insurance is the single most important risk management tool available to organizers, and the cost per participant makes it one of the most accessible.

| Point | Details |

|---|---|

| Two policies, not one | General liability and participant accident insurance cover different risks and both are needed. |

| Waivers have limits | Signed waivers do not protect against gross negligence claims; insurance covers those gaps. |

| Sanctioning unlocks coverage | Getting your event sanctioned is the first step to accessing comprehensive group insurance programs. |

| Costs are low | Event liability insurance runs as low as $0.15 per participant, with minimum premiums around $75. |

| Additional Insured matters | Landowners, municipalities, and sponsors must be named on your policy to secure most venue permits. |

The coverage gap most organizers don’t see coming

We have covered cycling events across Southern California and beyond for years at Socalcycling, and the insurance mistake we see most often is not a lack of coverage. It is the wrong kind of coverage. Organizers buy a general liability policy, assume they are protected, and never realize their participants have no medical cost support until someone gets hurt and files a lawsuit instead of a claim.

The second blind spot is the waiver overconfidence problem. We have watched organizers spend more time on their waiver language than on their insurance policy. Waivers are useful, but they are not a substitute for coverage. A well-drafted waiver and a solid insurance policy work together. One without the other leaves you exposed.

The third issue is the assumption that personal or club insurance transfers to event coverage. Many cyclists incorrectly assume home or club insurance covers racing events. It almost never does. Explicit examination of policy exclusions is the only way to know for certain.

Our advice: treat insurance as a line item in your event budget from day one, not an afterthought you address the week before the event. The cost is genuinely low. The risk of going without it is genuinely high.

— Socalcycling

Cycling event resources at Socalcycling

Socalcycling covers the full spectrum of cycling events, from Southern California road races to gravel rides and cyclocross series across North America.

For event organizers and participants looking to stay current on event formats, permit requirements, and race logistics, Socalcycling.com is the go-to resource. The site covers event calendars, race news, and practical guides that help organizers plan safer, better-run events. Whether you are organizing your first cycling sportive or managing a multi-day race series, the event coverage and guides at Socalcycling give you the context to make informed decisions at every stage of your planning process.

FAQ

What does cycling event liability insurance cover?

Event liability insurance covers third-party bodily injury and property damage claims made against the organizer. It pays legal defense costs and damages up to the policy limit, which commonly starts at a $2 million aggregate.

Do waivers replace the need for cycling event insurance?

No. Signed waivers do not protect organizers against gross negligence claims or incidents outside the inherent risks of the sport. Insurance covers the legal defense and damages that waivers cannot block.

How much does cycling event insurance cost per participant?

Event liability insurance costs as low as $0.15 per participant, with minimum premiums around $75. That makes it one of the most cost-effective risk management tools for any event size.

Does standard club or personal cycling insurance cover racing events?

Standard personal and club policies typically exclude racing and timed competitive events. Event-specific or sanctioned event insurance is required to fill that gap.

Who should be listed as Additional Insured on a cycling event policy?

Landowners, municipalities, and sponsors should all be listed as Additional Insured. Including these parties is a standard requirement for securing venue permits and protects all stakeholders connected to the event.

Recommended

- What Is a Cycling Passport Event? Your 2026 Guide

- Cycling Sportive Explained: Your Complete Ride Guide

- What Is a Cycling Omnium Event? Your Race Guide

- Cyclocross Race Calendar Checklist for 2026–2027

{kind=link}